{kind=link}

Great news from the crypto world in Europe: after years of waiting, the final MiCA text for regulation in the EU has finally been drafted, to be approved by the European Parliament as a last resort.

The text defines the guidelines that operators of cryptocurrency-related services will have to comply with in order to be regular.

Let’s take a look together at what the MiCA consists of and what the precise indications of the lawmakers are.

Crypto in Europe: what is MiCA?

These days the European Commission has drafted the final MiCA text for the regulation of all areas related to the world of cryptocurrencies in the EU, which will have to be approved by the European Parliament in order to finally enter into force.

In detail The MiCA (Market in Crypto Assets) represents the text indicating the regulations that EU service providers will have to comply with if they choose to adopt any kind of cryptocurrencies, whether NFTs, stablecoins or cryptographic tokens in general, into their business activities. There are also guidelines for cryptocurrency exchanges, which will have to follow certain rules to be regular throughout the EU.

The crypto community has been waiting for the final text of MiCA for years: the first proposal of the regulation was transcribed by the European Commission in September 2020.

Since then, given the complexity of the topics covered and the difficulty in framing the different cases of tokens linked to blockchain networks, there have been several slippages to reach approval in the final seat.

We have finally reached a turning point for crypto in Europe, where new laws will soon come into force that will allow providers of services linked to cryptographic tokens to operate in a fair and transparent way, without the fear of carrying out practices considered illegal.

Hence, no more gray areas and uncertainty about the future of cryptocurrencies in Europe.

This represents a turning point that will probably determine the boom of this sector in the EU, since many banks, investment funds and companies have chosen in the past years not to delve inside this world already unknown in itself and without precise guidelines at the legislative level.

However, even if the European Parliament approves the final text of the MiCA, it will be necessary to wait another 18 months for the compliance requirement to be triggered.

During this time, the regulation will have to be transcribed into more than 20 official EU languages and then published in the Official Journal.

The hope is that by 2024 cryptocurrencies will no longer be considered outlawed but an integral part of the current financial system with all the advantages and disadvantages attached.

MiCA’s crypto regulation in the context of NFTs, stablecoins and DeFi

Going into specifics, we can already get a glimpse of which categories of cryptocurrencies will fall under the MiCA regulatory framework.

In this regard, there is some news regarding the scope of NFTs, stablecoins and decentralized finance-related activities (DeFi).

Non-fungible tokens have definitely been the most delicate topic for regulators to deal with, as they had to frame them in the most appropriate way, without falling into the mistake of confusing them with different financial products compared to what they really represent.

Indeed, the previous draft of the regulation divided crypto-assets into three different categories, namely e-money tokens, utility tokens and asset-referenced tokens.

NFTs do not fall within any of these categories, as they are not tokens used for payments, as Bitcoin and Ethereum can be, nor are utility tokens and tokens that take back the value of other assets, such as stablecoins.

In the end, the European Commission decided that non-fungible tokens representing works of art, digital collections or real estate will not be part of MiCA regulation, hence will not be subject to the rules described in the text.

The only note to consider is the fact that if NFTs that are fractionalized or minted in series are issued, the latter will be considered fungible, hence appropriate as a means of payment, ergo they will be subject to requirements.

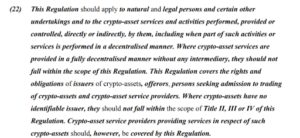

The same fate has befallen the decentralized finance sector that does not fall under European regulation.

This applies so long as there is the maintaining of effective decentralization of platforms where classic DeFi products such as liquidity providing, leverage trading and lending and borrowing of crypto assets will be offered.

In paragraph 22 of the text it can be clearly read that:

“where services are provided in a fully decentralized manner and without any intermediary, these rules do not apply.”

If, on the other hand, tokens tied to companies will be created, the latter will be required to obtain permits to be sold in Europe.

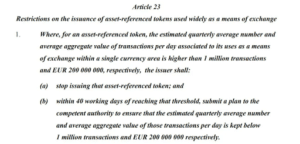

Finally, as far as stablecoins are concerned, these will have to follow precise rules:

The transaction volumes of stablecoins (not pegged to the euro) as a medium of exchange must remain below the quarterly average of EUR 200 million per day and 1 million transactions per day.

However, these limits do not apply to trading on exchanges.

If an operator exceeds the thresholds described, it will either have to stop providing such services or submit a plan to bring volumes back to regulatory levels.

New rules in EU for exchanges and financial service providers related to crypto

When it comes to cryptocurrency exchanges or more generally centralized crypto financial service providers, things get complicated.

The recent collapses of exchanges such as The Rock Trading or FTX have warned lawmakers against fully deregulating this type of platform.

The discriminating factor in understanding whether exchanges fall within the regulations is the “active marketing” factor, as described by Article 61.

Seeking to simplify: if service providers such as exchanges will carry out promotional activities in Europe to attract customers within their platforms, they will have to compulsorily register with a specific registry and report the conduct of their operations with the OAM, as specified by EU Directive 2018/843.

If, on the other hand, the exchanges will not do any marketing activities in Europe and customers choose of their own volition to use these services, the regulation does not apply.

Beware though, because this indication is meant to refer to operators based outside the European Union.

In fact, there are many exchanges that are based in the United States and also conduct their activities in Europe, such as Coinbase.

If an exchange is legally based in Europe, the previous regulations remain in place.

This represents a very interesting point to think about.

What will exchanges based outside Europe do now to increase their user base? Which activities will be considered active marketing and which will not?

Furthermore, what will new players who have planned to enter the industry as EU-based cryptocurrency exchanges do?

Will they decide to move their headquarters abroad or will they work to obtain all the necessary licenses to operate properly and transparently?

This last consideration cannot be answered concretely now.

The future will show us how the situation will evolve for the exchange industry in Europe and whether they will be penalized by the new MiCA regulation, assuming that it will be approved by the European Parliament.